articleSeven AI governance misconceptions holding your CX team back from achieving AI assuranceAmit Mishra • 5 minutes

articleLivePerson earns 22 G2 Spring 2026 badges, with top enterprise rankings across results, usability, and relationshipsCailyn Michaan • 5 minutes

articleHow synthetic customers became the non-negotiable assurance layer for enterprise AIStefanie Mazmanian • 7 minutes

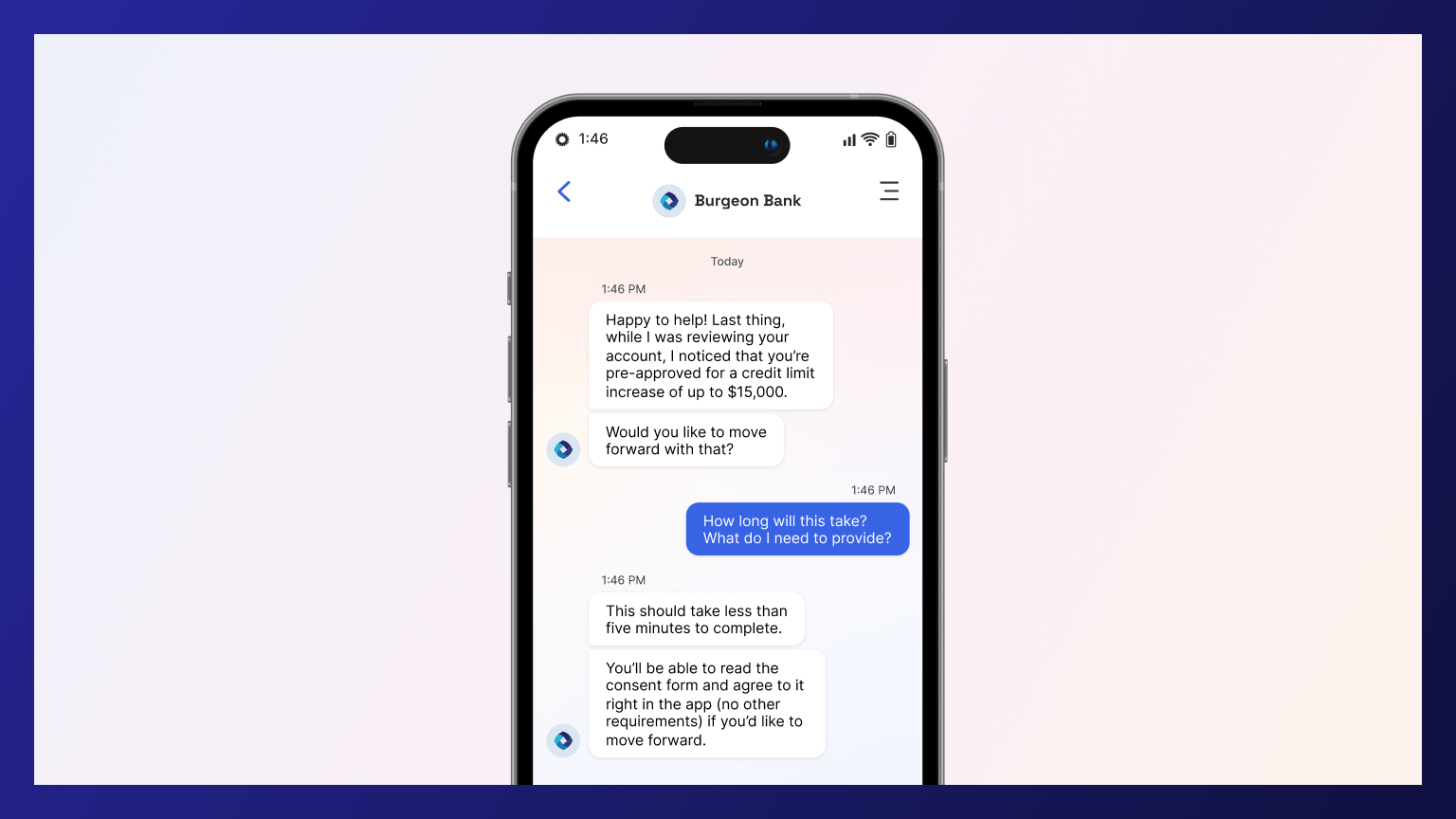

articleYou can’t scale what you can’t trust: Why enterprises must demand verifiable AINigel Lindsay-Smith • 4 minutes

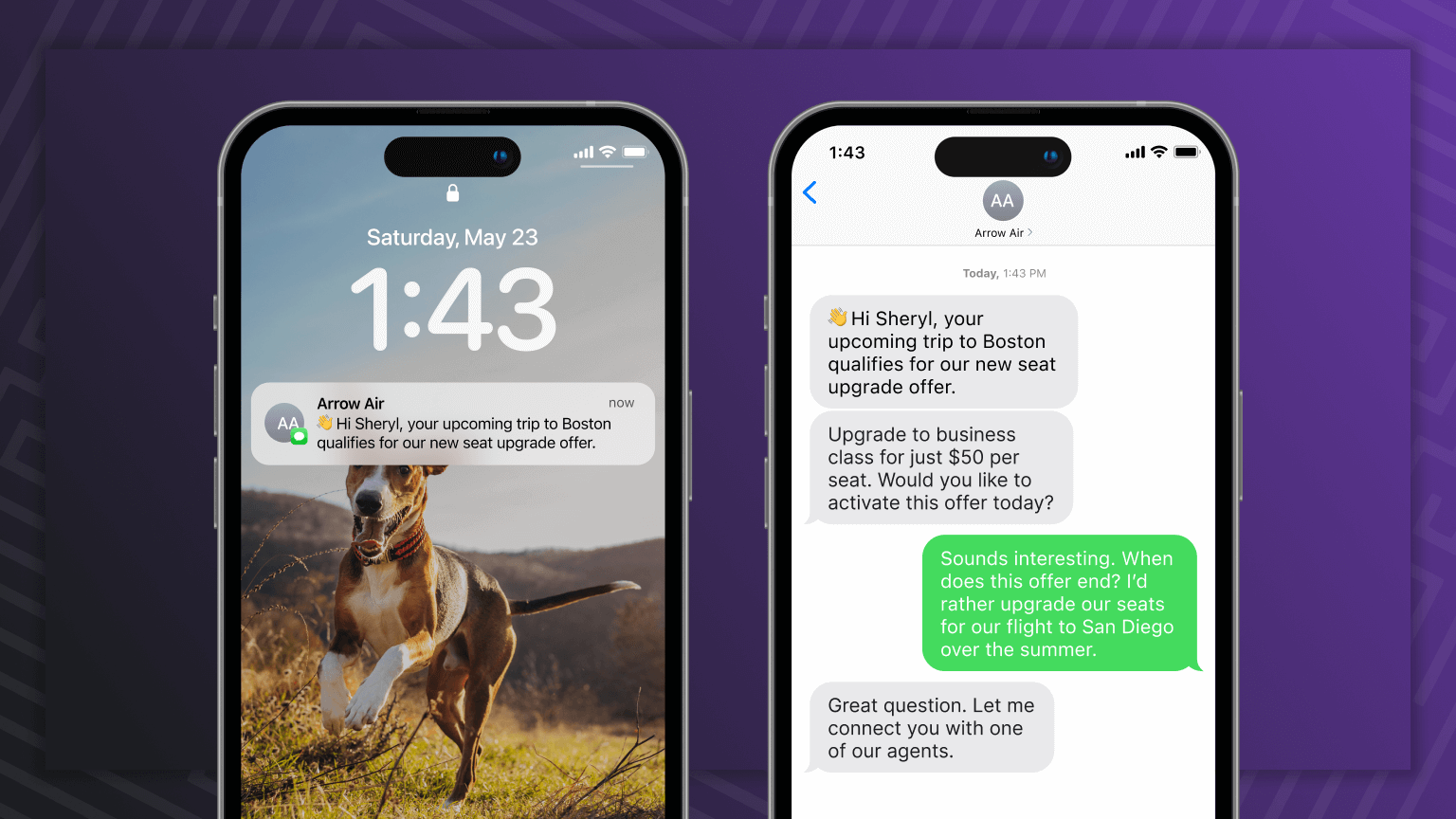

articleBeyond chatbots: How AI in customer service transforms support operationsMaia Capello • 9 minutes

articleMaximize contact center ROI with conversational AI for customer serviceMaia Capello • 5 minutes

articleHow proactive monitoring prevents enterprise crises before they happenMaia Capello • 3 minutes

articleWin the war for talent: Why digital employee experience drives retail successMark Scanlan • 5 minutes

articleGenerative AI for customer service: 5 essential takeaways for your contact centerRichard Steeves • 4 minutes

articleWhat are AI agents really — and why they’re reshaping the future of CXEthan Selfridge • 6 minutes

articleNet Promoter Score (NPS) survey template: What it is and why it mattersErica Richert • 5 minutes

article6 powerful chatbot examples: Transforming ecommerce and customer care in the digital ageCailyn Michaan • 6 minutes

articleTransforming the claims experience: A proven framework for insurance digital transformationAlex Ross • 8 minutes

articleLet’s talk about it: How conversations can drive telco digital transformationAlex Ross • 5 minutes

articleWhat is Conversational Commerce: How brands are using it to meet consumer demandAlex Ross • 5 minutes

articleHow to assist human agents and transform customer experience solutions with AIIttai Geiger • 6 minutes

articleBeyond the cloud: Exploring alternatives for AI-driven contact center digital transformationAlex Ross • 5 minutes

articleDesigning Jeanie: The story behind Fifth Third’s virtual banking assistantAlex Ross • 5 minutes

INFOGRAPHICOmnichannel contact center solutions to feed your customer service experienceAlex Ross • 5 minutes

articleFrom chatbots to AI agents: How to design purpose-built AI experiences with a human touchIttai Geiger • 8 minutes

articleVoice automation: The key to transforming routine conversations into contact center savingsMaia Capello • 4 minutes

articleCustomer interaction management: Navigating the complexity of omnichannel intentAlex Ross • 5 minutes

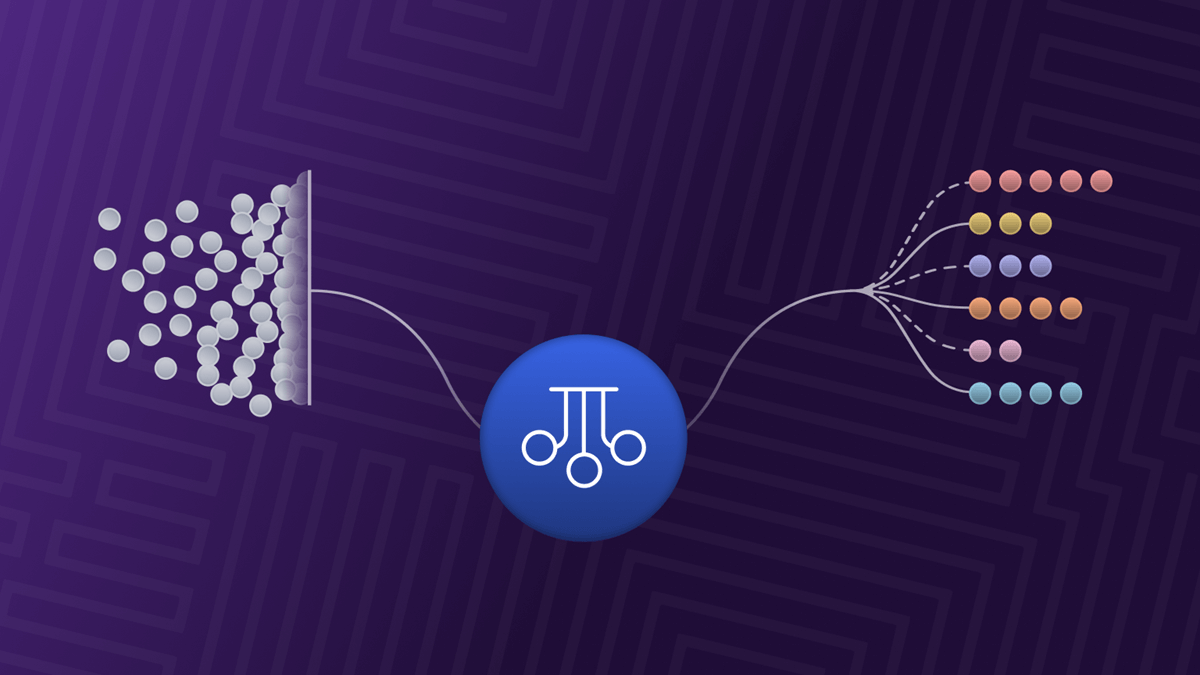

articleConversation Orchestration: Conducting a seamless customer service symphony through conversationsAli Malik • 9 minutes

articleHow to build a best-of-breed Contact Center as a Service (CCaaS) solutionMaia Capello • 5 minutes